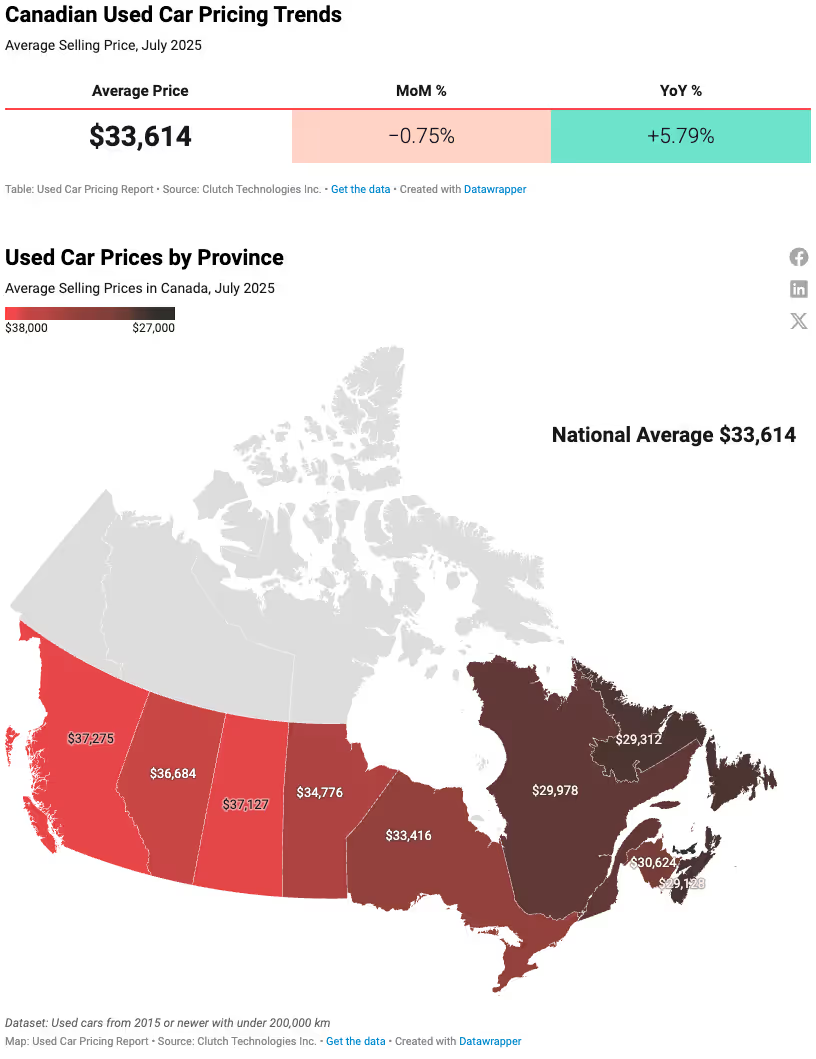

Canada’s used-vehicle market edged down in July, with the average transaction at $33,614, a 0.75% dip from June yet still 5.79% above last year. That cooling coincided with a significant labour market shift: Canada shed more than 40,000 jobs during the month, bringing the employment rate to its lowest point since the pandemic. It’s hard to ignore the potential link between that weaker job market and softer used-car prices, especially for buyers facing tighter budgets.

SUVs continued to claim a larger share of what Canadians bought in July, yet their average prices stayed steady as more shoppers opted for budget-friendly crossovers like the Nissan Rogue, Chevrolet Equinox, and Ford Escape. At the same time, full-size pickups such as the Ford F-150, GMC Sierra 1500, and Chevrolet Silverado 1500 held firm on pricing, which helped keep the national average from sliding further. It’s a push-and-pull dynamic that long-time market watchers will recognize from other economic slowdowns: practical, affordable choices offset by the pricing power of high-demand workhorses.

Regional nuances make the picture even more interesting. Québec is still the most affordable province overall, but it has seen the sharpest year-over-year deterioration in affordability. British Columbia remains a solid hunting ground for reasonably priced SUVs, while Ontario continues to see affordability pressure from trucks holding their value. Meanwhile, in EVs, the momentum continues to shift toward crossovers like the Tesla Model Y and Mustang Mach-E, which are nudging provincial averages but still represent a small slice of the national market.

British Columbia and Saskatchewan top the provincial price table this month, each averaging just over $37,000. At the other end, Prince Edward Island sits below $28,200, marking a gap of nearly $9,000 from the leaders. Month-over-month, the picture is far from uniform. Manitoba and New Brunswick posted the largest jumps, up 1.96% and 4.83% respectively, while Alberta saw a notable 2.85% drop. Year-over-year, Québec stands out with a 10.55% increase despite remaining one of the lowest-priced markets.

In the West, trucks continue to define pricing. British Columbia’s average slipped only 0.44% from June, a sign that steady SUV demand is being matched by supply at consistent price points. Alberta’s sharper drop suggests more than seasonal easing; shifts in the mix of vehicles sold, particularly fewer high-priced pickups, may have pulled the average down. Saskatchewan’s dip of 1.20% is smaller but comes off an already high base.

Central Canada shows its own split personality. Ontario’s average fell 1.02% MoM but remains elevated, supported by strong pricing in the full-size pickup segment. Québec’s story is different: still the cheapest market, yet prices there have climbed at twice the national YoY pace, driven in part by growth in higher-priced truck and EV sales.

Atlantic Canada’s lower absolute prices mask some affordability erosion. New Brunswick, for example, is up nearly 6.15% YoY, and the proportion of trucks under $30,000 has slipped. Nova Scotia moved in the opposite direction month-to-month, down 1.82%, showing how the availability of compact SUVs can swing affordability in smaller markets.

Over the last year and a half, national used-vehicle pricing followed a distinct arc: a slower start through early 2024, a sustained climb over seven straight months, and then a July pullback to $33,614—down 0.75% from June but still 5.79% above last year. This pause came in a month when Statistics Canada reported over 40,000 jobs lost and employment dropping to 60.7%, the lowest point since July 2021. That labour softness landed alongside a rebound in consumer confidence through the spring and summer, according to the Conference Board of Canada, though both remain well below pre-inflation highs. In practical terms, it’s a market where optimism exists, but it’s still fragile—and that usually means more appetite for value segments and tighter limits on monthly payments.

Segment dynamics amplified those macro effects. Full-size pickups maintained high late-model transaction prices, keeping the national average from falling further. In contrast, mainstream compact crossovers—helped by steady supply and new-car promotions on current model years—tempered the climb by holding their used prices steady.

EV pricing told a more regional story, reflecting incentive changes in 2025: Québec’s reduced Roulez-vert rebates in April, B.C.’s Go Electric pause in May, and the federal iZEV program on hold since January. These shifts produced pockets of volatility in provincial EV averages but little change to the national curve. The result is a line that looks like a plateau after months of gains, shaped by resilient truck prices, stable SUV values, and a consumer base that is cautiously optimistic but still price-sensitive.

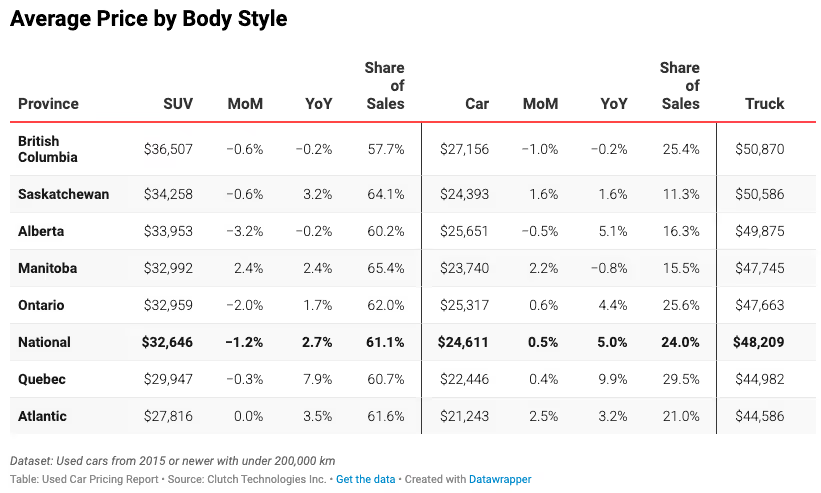

SUVs remain the dominant force in Canada’s used-vehicle market, now accounting for 61.1% of transactions—up 2.6 pp YoY and 2.1 pp MoM. That sales share growth alone contributed about one-fifth of the national average price lift over the past year, but the bigger driver was what happened inside the segments themselves. Trucks, in particular, delivered most of the dollar gain, with late-model F-150s, Sierras, and Silverados commanding transaction prices that are up 9.0% YoY and 2.1% MoM.

Cars, despite losing 3.3 pp of share YoY, have edged higher in value. Average prices climbed 5.6% YoY and 1.5% MoM, led by the Civic and Corolla, both of which held or expanded share while posting meaningful price gains. This suggests demand resilience for proven, fuel-efficient sedans even as buyers lean toward SUVs.

In BC, Alberta, and Ontario, value-oriented compact SUVs—Rogue, Equinox, Escape—are key to the share story. In BC, SUV share inched up 0.4 pp YoY to 57.7%, yet the segment average slipped 0.4% YoY and 0.1% MoM to $36.5 k, as share gains came from lower-priced nameplates. Ontario’s SUV share rose 3.3 pp YoY to 61.9%, with pricing up just 1.7% YoY and flat MoM at $33.0 k; the Rogue’s share growth alone helped cap segment inflation by roughly $400. In Alberta, SUV share growth mirrored Ontario’s, with prices up less than 2% YoY, also anchored by cost-efficient compacts.

Québec shows how a small truck base can magnify price effects. Trucks now hold 9.7% share (+1.6 pp YoY), with average prices surging 11.2% YoY (+$4.5 k) and 0.9% MoM. Car share fell 2.1 pp YoY, but prices climbed 9.9% YoY and 1.3% MoM, driven by higher pricing on Sentra, Civic, and Corolla. SUV share is steady at about 61%, with prices up 7.9% YoY and 0.5% MoM.

The Atlantic provinces illustrate a different balance. Nova Scotia and Newfoundland and Labrador saw SUV share rise but segment prices move less than 1% YoY. PEI’s higher truck share delivered a sharper average-price rise of 4-6% YoY, despite modest MoM changes.

At the model level, share and price shifts are often working against each other. The CR-V has kept both MoM and YoY prices steady while maintaining a top-five share position in most provinces, meaning it adds volume without inflating averages. By contrast, the Rogue and Equinox have gained share from higher-priced competitors, pulling down segment averages even as they help SUVs take a larger slice of the market. Trucks show the opposite dynamic—share gains tend to come from pricier trims, amplifying both segment and overall price movements.

National Fuel-Type Trends

Gasoline vehicles remain the backbone of Canada’s used-vehicle market at close to 91% share, but electrified powertrains (EVs and hybrids) are where the most notable pricing and mix changes are occurring. In July, gasoline vehicle prices were essentially flat month-over-month at the national level, with mixed provincial moves—Alberta (-1.9% MoM) and B.C. (-0.6% MoM) down slightly, Québec up 0.4%. Year-over-year, gasoline vehicle pricing is still higher in most provinces, supported by strength in full-size pickups within the gas segment. This within-segment truck lift helps explain why the national overall price stayed stable in July despite electrified-segment softness.

Hybrids posted a July MoM national pricing decline, largely driven by price drops in Québec (-6.0%) and Ontario (-1.6%), partially offset by a small B.C. gain (+1.2%). The YoY picture is more positive—hybrid prices are still higher than a year ago in many provinces—but the monthly dip points to short-term discounting and mix shifts toward lower-priced hybrid models.

EVs saw the sharpest national MoM drop, driven by Ontario’s 6.1% decline and its outsized weight in the EV market. Québec (+1.5% MoM) and B.C. (+0.1%) both rose slightly, but their increases were not enough to counter Ontario’s pull. YoY, EV prices are down in most provinces, even in cases where higher-priced models are taking share.

Model Share vs. Price Dynamics

Across all three fuel types, the interplay between what people are buying (sales share shifts) and what those vehicles cost (within-model price changes) is crucial. In gas, stable segment pricing hides underlying gains in late-model trucks and pullbacks in compact-SUV prices. In hybrids, part of the July decline came from share gains in value-oriented models, which pulled the average down despite steady prices on some higher-priced hybrids.

The EV market shows the most striking divergence between share and price. In B.C. and Québec, premium models such as the Tesla Model Y, Model 3, Ford Mustang Mach-E, and even electric pickups like the F-150 Lightning are replacing legacy compacts like the Nissan Leaf and Chevy Bolt in the sales mix. In Québec, that shift alone added over $4,000 to the average EV price, even though those same premium models saw within-model price cuts of $3,000-$8,000. In B.C., mix gains from Teslas and Lightning offset 70% of a $5,100 price decline from within-model markdowns. Ontario’s mix effect was nearly neutral—the rise in Teslas and Mach-E was balanced by declines in similarly-priced Korean and Japanese EVs—so its $7,300+ price drop was almost entirely within-model.

Overall, gas keeps the market’s baseline steady, hybrids are showing early signs of price softening, and EVs illustrate how a market can “upgrade” in mix while still becoming cheaper on a per-model basis. If EV within-model cuts persist, the premium-mix cushion seen in B.C. and Québec could erode quickly.

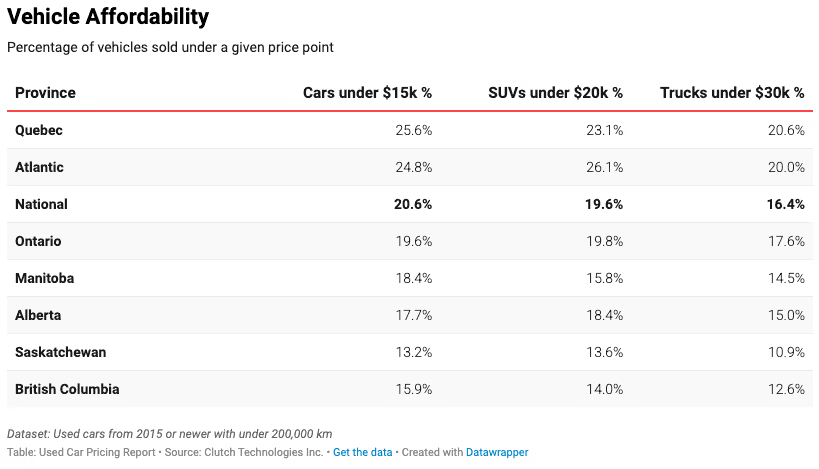

In July 2025, the affordability picture for Canadian used vehicles continued to slip, with national shares of entry-level vehicles now sitting at 20.6% for cars under $15k, 19.6% for SUVs under $20k, and 16.4% for trucks under $30k. The gap between cars and trucks in particular underscores where the squeeze is most acute—late-model pickups have simply outpaced the caps.

Cars remain the most accessible segment in relative terms, but even here, availability is eroding. Québec leads the country with 25.6% of car sales under $15k, yet that position masks sharp year-over-year declines. High-volume compacts like the Civic and Corolla have crept up in price, while low-cost anchors such as the Hyundai Accent are no longer expanding their footprint. Saskatchewan sits at the other end of the spectrum with just 13.2% of cars under $15k, reinforcing how local mix and pricing power shape the bottom line.

SUV affordability is holding up better where value crossovers are plentiful. Atlantic Canada tops this category at 26.1%, largely thanks to the steady presence of sub-$20k Escapes and Rogues. British Columbia has also carved out gains here—up from 13.6% last month—despite the province’s high overall price level.

Trucks remain the biggest pressure point. Even Québec, the national leader at 20.6% under $30k, has seen notable slippage as F-150, Sierra 1500, and Silverado 1500 prices creep past the threshold. Ontario’s affordable-truck share has fallen to 17.6%, the third-steepest drop nationally, echoing the $5k YoY pickup price lift seen earlier in the pricing data. Saskatchewan is now the least affordable truck market at just 10.9% under $30k.

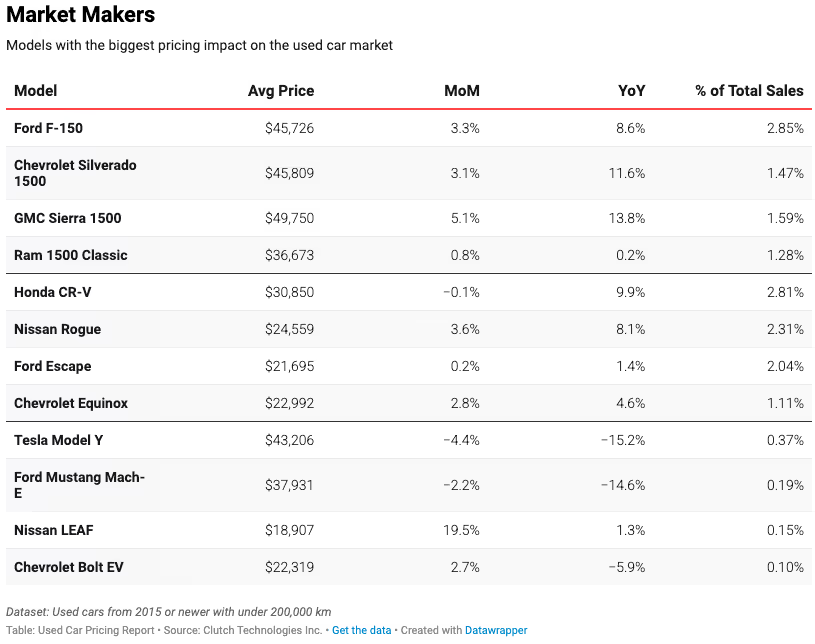

July’s leaderboard shows a familiar set of faces, but the shifts inside the top 10 still tell a lot about the market’s underlying currents. The Honda Civic and Toyota Corolla continue to anchor the compact-car category, each holding around 2.8-1.5% of national sales. Both managed modest price lifts—Civic up 2.0 % MoM, Corolla up 1.3%—despite the broader slide in car share. That stability hints at sustained demand for higher-quality compacts, even as cheaper options fade.

SUVs continued to dominate the rankings in July, but the internal order shifted in a way that underscores the market’s tilt toward more affordable options. The Nissan Rogue leapfrogged the Toyota RAV4 to claim the higher spot, riding a +0.39 pp MoM share gain and holding an average price roughly $6,500 below the RAV4. That swap in the standings is emblematic of what’s happening across the segment: compact SUVs that sit well under the national SUV average are picking up speed. The Kia Sportage, Jeep Compass, and Kia Seltos all posted notable share gains this month, reinforcing the idea that buyers are chasing approachable price points without leaving the SUV category. This affordability-driven momentum is keeping overall SUV prices in check even as the segment’s share of national sales expands. The trend also dovetails with what we saw provincially—BC, Alberta, and Ontario all registered SUV share growth fuelled by these same value-oriented models.

In the truck space, Ram 1500 and GMC Sierra 1500 both added share in July—+0.11 pp and +0.15 pp respectively—while posting strong MoM price gains (5.8% and 5.1%). Their moves reinforce the truck-driven lift in national averages we saw in the body-style analysis. Yet outside the top 10, the Ram 1500 Classic’s -0.27 pp share loss shows not all pickups are riding the same wave; affordability caps are cutting into entry-level truck volumes.

The middle of the rankings also hides a few provincial tells. The Nissan Sentra’s +0.16 pp share gain (and $19,299 average price) matches the trend in Ontario and Québec toward budget-friendly gas sedans as some buyers pivot away from higher-priced SUVs. Likewise, the Volkswagen Atlas’s -0.11 pp drop reflects waning appetite for pricier mid-size SUVs in markets where affordable compact-SUV options are plentiful.

Even within this static-looking top 10, the mix of price moves and share shifts points to a market balancing two forces: upward pressure from trucks and select SUVs, and competitive pricing in smaller segments keeping a lid on the national average.

Own one of these top-selling models? See in-depth pricing insights with our Car Value Calculator.

July saw the compact-SUV trio of Nissan Rogue, Chevrolet Equinox, and Ford Escape continue to expand the affordable compact footprint in national SUV sales, collectively adding meaningful points without imposing heavy price inflation. The Rogue’s 2.31% share (+0.12 pp MoM) kept its average price at $24.6k (+3.6% MoM), reinforcing its position as an accessible anchor for the segment. Equinox posted 1.11% share (+0.06 pp MoM) at $23.0k (+2.8% MoM), maintaining the “value SUV” profile. Escape, while dipping slightly in share to 2.04% (-0.09 pp), held steady on pricing at $21.7k (+0.2% MoM). Together, these models illustrate why SUV share can rise in the aggregate without sparking an outsized price spike—more affordable models keep the segment’s entry points intact even as volumes grow.

The Honda CR-V continues to play a stabilizing role in the compact-SUV space. At 2.81% share (-0.25 pp MoM) and an average price of $30.9k (-0.1 % MoM), it remains one of the most consistently priced high-volume models in the market. However, it gave up market share to models in the value-SUV cohort, which helped the overall SUV segment tick down in price for the month.

The big three full-size trucks again demonstrated their role as the market’s price engine. Ford F-150 led the way with a 2.85 % share (-0.40 pp) at $45.7k (+3.3% MoM). GMC Sierra 1500 showed the strongest price lift at +5.1% MoM to $49.8k, despite a small share dip (-0.05 pp). Chevrolet Silverado 1500 mirrored these patterns at $45.8k (+3.8% MoM). In contrast, the Ram 1500 Classic, still the most budget-friendly at $36.7k, edged up just 0.8% in price, but fell sharply in share (-0.50 pp), reducing its moderating influence on the sub-$30k truck market.

The EV segment’s internal reshuffle continued, with crossover EVs overtaking legacy compact EVs. The Tesla Model Y increased its EV-segment footprint and held pricing in the low-$40k range, while Ford Mustang Mach-E also climbed in share at $38.0k. The prices for these two have dropped astronomically over the last year, making for a great opportunity for any shopper in search of an affordable premium EV. In contrast, the Nissan Leaf and Chevrolet Bolt EV receded in market share. This shift toward crossovers helps explain provincial EV trends where higher-priced models soften the average price drop by replacing lower-priced compacts in the mix.

{{widget-1}}

The Hyundai Elantra continues to dominate the entry-car space, holding nearly 10% of all sales in this band and cementing its status as the affordability anchor in the Prairies and Atlantic, where its share runs several points higher. The Chevrolet Cruze leapfrogs the Civic into second, buoyed by broad availability across central provinces and a pricing profile that consistently clears the $15k cap. Honda Civic and Toyota Corolla remain visible in some provincial affordability tables, but for July, their national shares lagged as higher trim mixes crept into the listings. Kia Forte and Mazda3 round out the list, each holding a 4-5% share with stable volumes.

Ford Escape and Nissan Rogue do most of the heavy lifting in keeping compact-SUV affordability alive, combining for over 14% of the <$20k SUV market. Chevrolet Equinox edged past Jeep Cherokee into third place nationally, illustrating the trend toward lower-priced domestic crossovers in British Columbia, Alberta, and Ontario. Kia Sportage posted a solid gain, aligning with our broader compact-SUV share climb, while the Hyundai Kona—despite its sub-compact footprint—saw its <$20k share dented in markets like Atlantic Canada where price spikes pushed many units above the cap.

Ram 1500 leads the affordable-truck category at 24.10% of <$30k transactions, followed by the Ford F-150 at 20.40%. The GMC Sierra 1500 climbed two ranks in July to 11.62% share, narrowly ahead of the Chevrolet Silverado 1500 at 11.58%. The Ram 1500 Classic rounds out the top five at 11.54%, though its -2 rank change signals a softer showing compared with June. Together, these five models make up nearly 80% of all <$30k truck sales, underscoring how concentrated affordability has become in this category.

Looking for one of these high-demand picks? Browse our affordable inventory at Clutch — every vehicle is fully inspected, reconditioned, and backed by a 10-day money-back guarantee.

Final Takeaways & What to Expect Next

July’s data points to a market still shaped by compact-SUV momentum and a shifting EV mix. Value-leaning crossovers like Rogue, Equinox, and Escape are allowing SUVs to expand their share without creating broad upward pressure on segment prices. But with SUV share increasing in the national sales mix, even stable prices in this category will push the overall market average higher over time, given SUVs’ higher baseline prices compared to cars.

In the EV segment, crossovers such as the Model Y and Mach-E continue to gain share at the expense of legacy compacts like the Leaf and Bolt EV. What’s striking is that this shift toward more premium body styles is happening alongside ongoing model-level price reductions. The result is a widening gap between EV sub-segments: higher-volume crossovers are anchoring the share story, while lower-priced compacts are losing both volume and pricing power.

Consumer sentiment and interest rate uncertainty remain important watchpoints. The Bank of Canada’s policy path into year-end is still unclear, with any shift in rates likely to influence payment tolerances and, by extension, used-market transaction patterns. At the same time, we’re watching for possible price firming in the new-car market this fall. With 2026 model-year tariff-related increases expected to filter through OEM price lists, any upward move in new-car MSRPs could reinforce used-market price floors—particularly in high-demand segments like compact SUVs and EV crossovers.

Taken together, these dynamics suggest that, barring a major shift in consumer sentiment or inventory conditions, the combination of rising SUV share, steady EV crossover gains, and potential tariff-driven new-car price pressure is likely to translate into continued, moderate price increases in the used market through late summer and into the fall.

About This Data

This report is based on Clutch’s internal data, collected from retail vehicle sales reported across Canada. The analysis includes vehicles that meet the following criteria:

- Model year 2015 or newer

- Less than 200,000 km at the time of sale

- Sold vehicles only

References to “cars” include both sedans and hatchbacks, while SUVs and trucks are categorized separately. This segmentation helps reflect real-world buyer preferences across different body styles.

While the dataset covers a large national sample, pricing in smaller provinces or regions with lower sales volume may be influenced by individual outliers. This can lead to greater month-over-month fluctuations in certain areas compared to larger markets like Ontario, Quebec, and British Columbia.

The figures presented reflect average asking prices at the time of sale and are designed to provide an accurate snapshot of current market trends.

.avif)

-02.avif)